The Time Value of Prime Time: The $177M Olympic Broadcast Bid

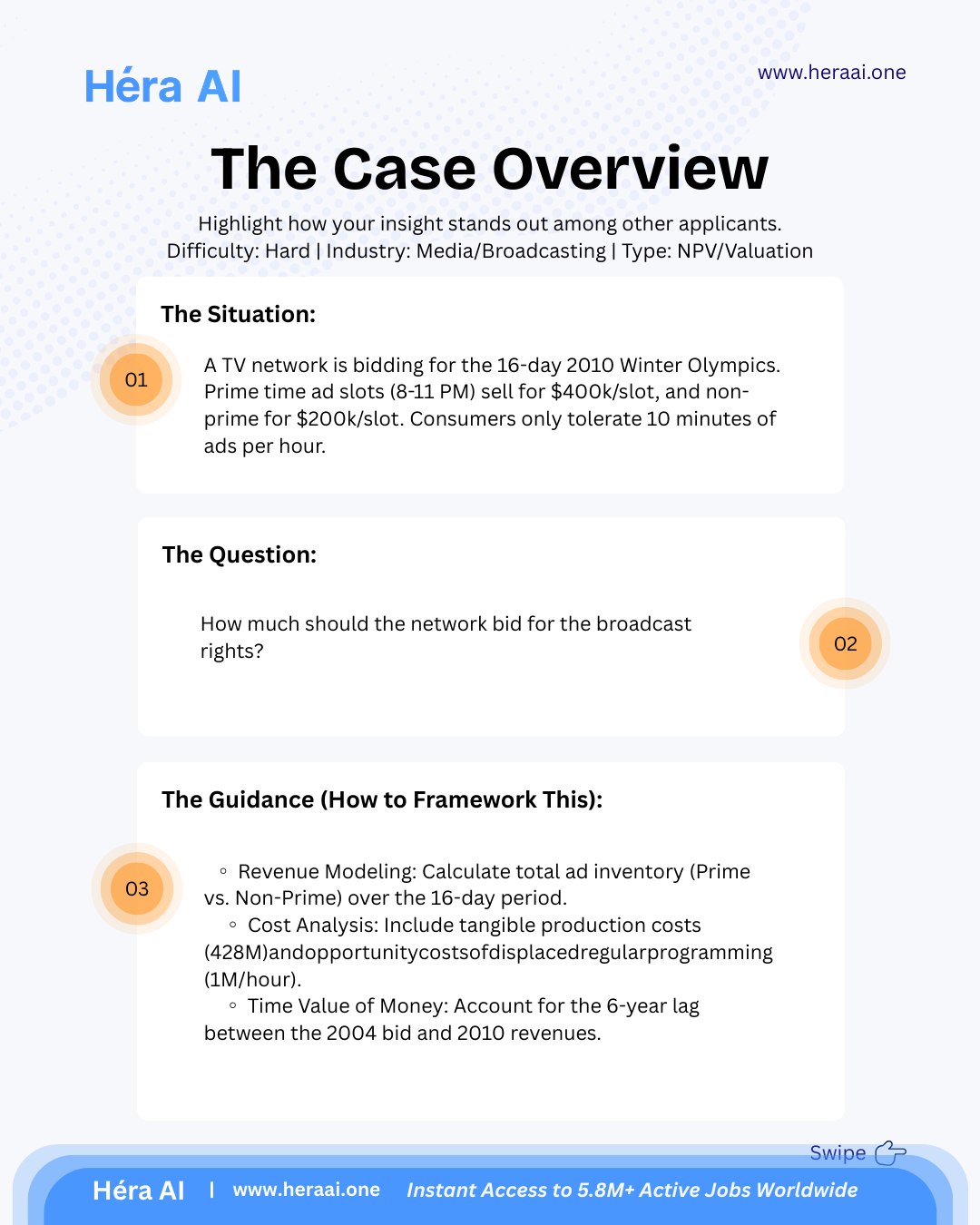

A TV network bidding in 2004 for the 2010 Winter Olympics. Three financial traps, one strategic recommendation, and the question every consulting interviewer is really asking.

Most candidates who see an Olympic broadcast case think: revenue minus costs. The interviewers know this. The case is designed to expose the three layers of financial reasoning that separate that first instinct from a senior-level recommendation: opportunity cost, time value of money, and the discipline to know when to bid above your own NPV calculation — and why.

This is Case 30 in HéraAI's Case Strategy Chamber series. The scenario: you're the CFO of a major TV network bidding in 2004 for the rights to broadcast the 2010 Winter Olympics — a 16-day event. The IOC wants a bid. You have a week to build the model and make the recommendation. Here is how a top-tier consulting candidate structures it.

How to Structure This Case: The Three-Layer Framework

A media rights valuation case has three analytical layers, each of which is a separate failure point in an interview. The first layer — building the revenue model — is where most candidates focus all their preparation. The second layer — opportunity cost — is where approximately 70% of candidates fail on first pass. The third layer — discounting to present value — is where the senior-level filter operates.

Step 1 — Building the Ad Inventory Model

Revenue in broadcast is a function of two variables: the price per ad slot and the number of slots available. Both are constrained. Consumer research establishes that audiences tolerate approximately 10 minutes of advertising per hour before engagement drops significantly — which translates to 6 thirty-second slots per hour. Price varies by daypart: prime time (8–11pm) commands $400k per slot; non-prime carries $200k.

The broadcast schedule covers 16 days: 10 weekdays, 4 weekend days, the Opening Ceremony, and the Closing Ceremony. Ceremonies are full prime-time events. The table below models the slot inventory across the full broadcast window.

Scaling the slot model to total gross revenue requires assumptions about the full broadcast day — not just the evening window modeled above. A full 16-day Olympic schedule includes approximately 15 hours of coverage per day across prime and non-prime dayparts. The total gross ad revenue, across all markets and daypart segments, reaches approximately $928M before costs.

The precision signal: In a case interview, candidates are not expected to produce the exact number — they are expected to demonstrate a logical, structured approach to estimation. Walking through the slot calculation tier by tier, naming the assumptions explicitly (6 slots per hour, prime vs. non-prime segmentation, ceremony premium), and arriving at a defensible order-of-magnitude estimate is more valuable than a precise figure reached through opaque reasoning.

Step 2 — The Opportunity Cost Trap

Broadcasting the Olympics is not revenue with no cost beyond production. It displaces content. Every hour of Olympic coverage is an hour in which the network is not broadcasting its regular schedule — which already generates approximately $1M per hour in ad revenue from established programming. This is the opportunity cost of the bid, and it is the most commonly missed component in media valuation cases.

The displacement runs across approximately 154 hours of the broadcast window — the overlap between Olympic coverage hours and the network's existing primetime and daytime schedule. At $1M per hour, the opportunity cost is $154M. This is not a production expense. It is the revenue that the network gives up by showing the Olympics instead of its regular content.

Why this is the most important number in the case: The opportunity cost argument is what transforms this from an accounting exercise into a strategic one. A network with weak regular programming has a lower opportunity cost and a higher willingness to pay for rights. A network with strong primetime ratings faces a real trade-off between the Olympic halo effect and the disruption to its regular audience. Surfacing this dimension — without being asked — is the clearest signal of commercial judgment in this case type.

Step 3 — The Full P&L and NPV Calculation

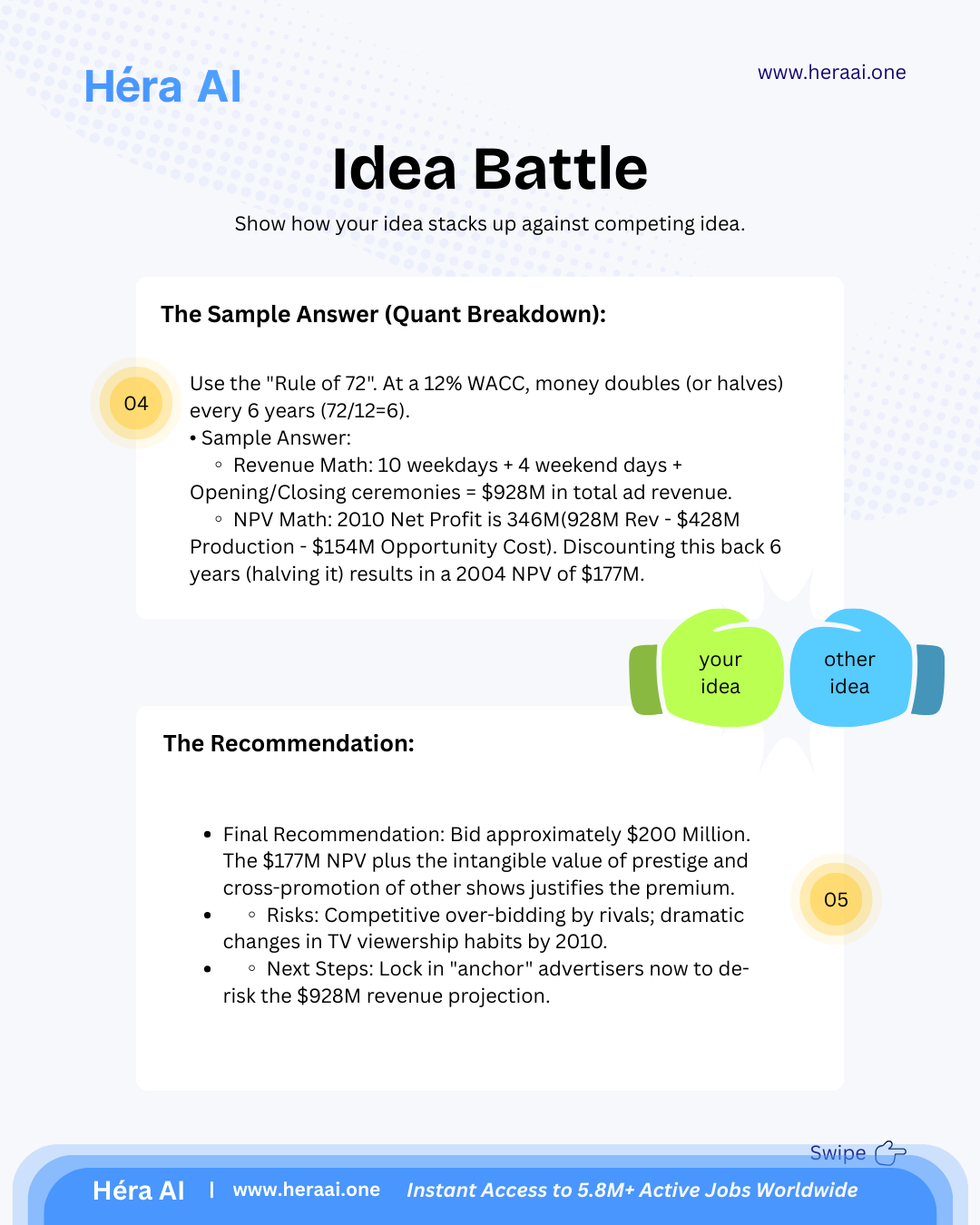

With gross revenue modeled and all costs identified, the P&L waterfall builds cleanly. The critical final step is discounting the 2010 net profit back to 2004 present value — the year of the bid. A 12% WACC applied over six years produces a discount factor of approximately 0.51, using the Rule of 72 as a mental model: at 12%, capital doubles every six years, meaning future cash flows are worth roughly half today.

The Rule of 72 is not a substitute for a precise DCF calculation — but it is exactly the kind of rapid approximation that case interviewers reward. Being able to say 'at 12% WACC, the Rule of 72 tells me this profit stream roughly halves over the six-year lag, giving us approximately $177M in today's dollars' demonstrates both financial fluency and the ability to reason quickly without a spreadsheet.

The number that the bid must be anchored to: $177M is the NPV floor — the point below which the investment creates value, and above which it destroys it on a pure financial basis. This is not the recommended bid. It is the analytical ceiling for the financial argument. The strategic recommendation builds from here.

Step 4 — The Strategic Recommendation: Why $200M

The final output of this case is not a number. It is a recommendation with a justification. The NPV says the financial value of the broadcast rights, in 2004 dollars, is $177M. The recommendation is to bid $200M. The $23M difference — approximately 13% above NPV — requires a specific, defensible argument. In this case, there are two.

The discipline the recommendation requires: the prestige premium argument must be bounded. Candidates who argue for bidding $300M 'because the Olympics is priceless' have abandoned analytical reasoning for strategic hand-waving. The correct answer acknowledges the specific, quantifiable channels through which the premium creates value — and sets a limit on how far above NPV a rational bid can go.

Step 5 — Risk Assessment

No bid recommendation is complete without a risk frame. This case was set in 2004 for a 2010 event — a period that bridged a significant structural shift in how audiences consumed television. The risk register below captures the factors that could cause the realized return to fall below the modeled NPV.

The viewing habit shift risk deserves specific attention because it is structural rather than probabilistic. By 2010, DVR penetration had reached approximately 40% of US households, and online streaming was beginning its early-stage growth. A model built on 2004 linear TV economics was already discounting a structural trend that would accelerate significantly in the following decade. The sophisticated candidate acknowledges this explicitly and suggests that the model should incorporate a downside scenario with a 10–15% audience discount to test the bid's robustness.

The Five-Step Interview Framework

The table below consolidates the full case approach into an interview-ready structure. Each step includes the action, the common trap, and the framing that separates a good answer from a great one.

The meta-principle this case tests: A bid is not an NPV calculation. It is a judgment call about risk appetite, competitive dynamics, and the value of intangibles — anchored by an NPV calculation. Candidates who treat the math as the conclusion have misunderstood the question. Candidates who ignore the math in favor of strategic intuition have also misunderstood the question. The answer that wins is the one that does both: rigorous quantitative foundation, strategically intelligent recommendation built on top of it.