Case 15: Should We Drop $700M on a Wind Turbine Company?

The math says $750M. The asking price is $700M. On paper it looks like a deal. What the model does not show is everything that can make $750M become $500M — and why the $50M buffer is thin.

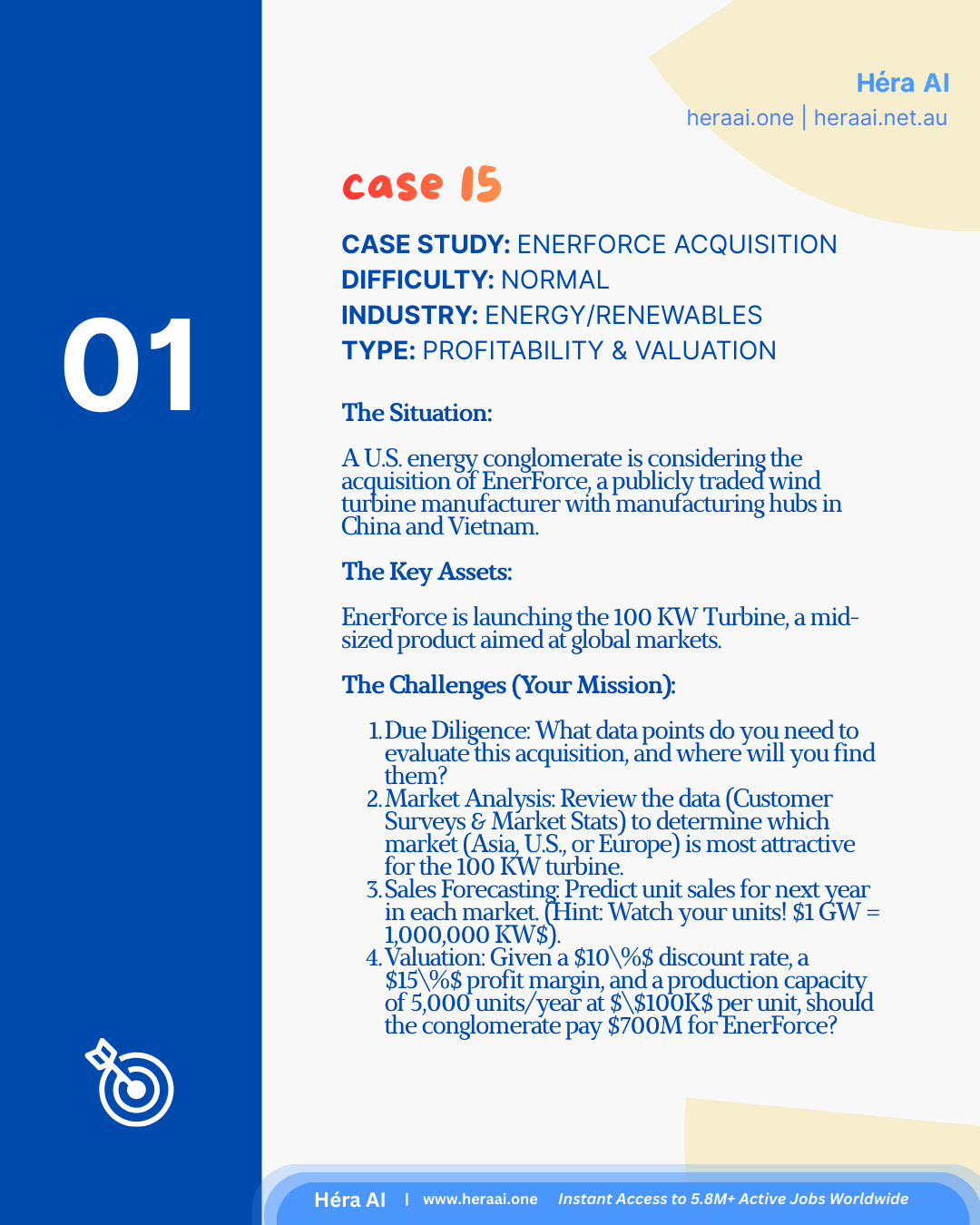

Case 15 is an M&A valuation case set in the renewable energy sector — a category that combines quantitative rigour with geopolitical judgement in a way that tests both the financial modelling instincts and the strategic awareness of the candidate. The client is a U.S. energy conglomerate evaluating an acquisition of EnerForce, a publicly traded wind turbine manufacturer with production facilities in China and Vietnam. The asking price is $700M. The question is whether to pay it.

The case contains two traps and one decisive insight. The first trap is the unit conversion: 1 gigawatt equals one million kilowatts, and a candidate who misses this conversion when sizing the addressable market will produce a revenue estimate that is off by a factor of one thousand. The second trap is the market assumption: treating Asia and Western markets as equivalent addressable opportunities when they are, in fact, fundamentally different competitive environments with different share potential for EnerForce's product.

The decisive insight is the market differentiation between Asia and the U.S./Europe. Asia competes on cost per kilowatt-hour generated — a metric where EnerForce, manufacturing in China and Vietnam, cannot compete with domestic producers who benefit from local subsidies and lower structural costs. The U.S. and Europe, by contrast, value turbine aesthetics, supplier reliability, and Western manufacturing credibility — dimensions where EnerForce's 100 KW turbine has a genuine and defensible advantage. This insight determines the market share assumptions, which determine the revenue projection, which determines the valuation.

Due Diligence: What to Ask Before the Valuation Model

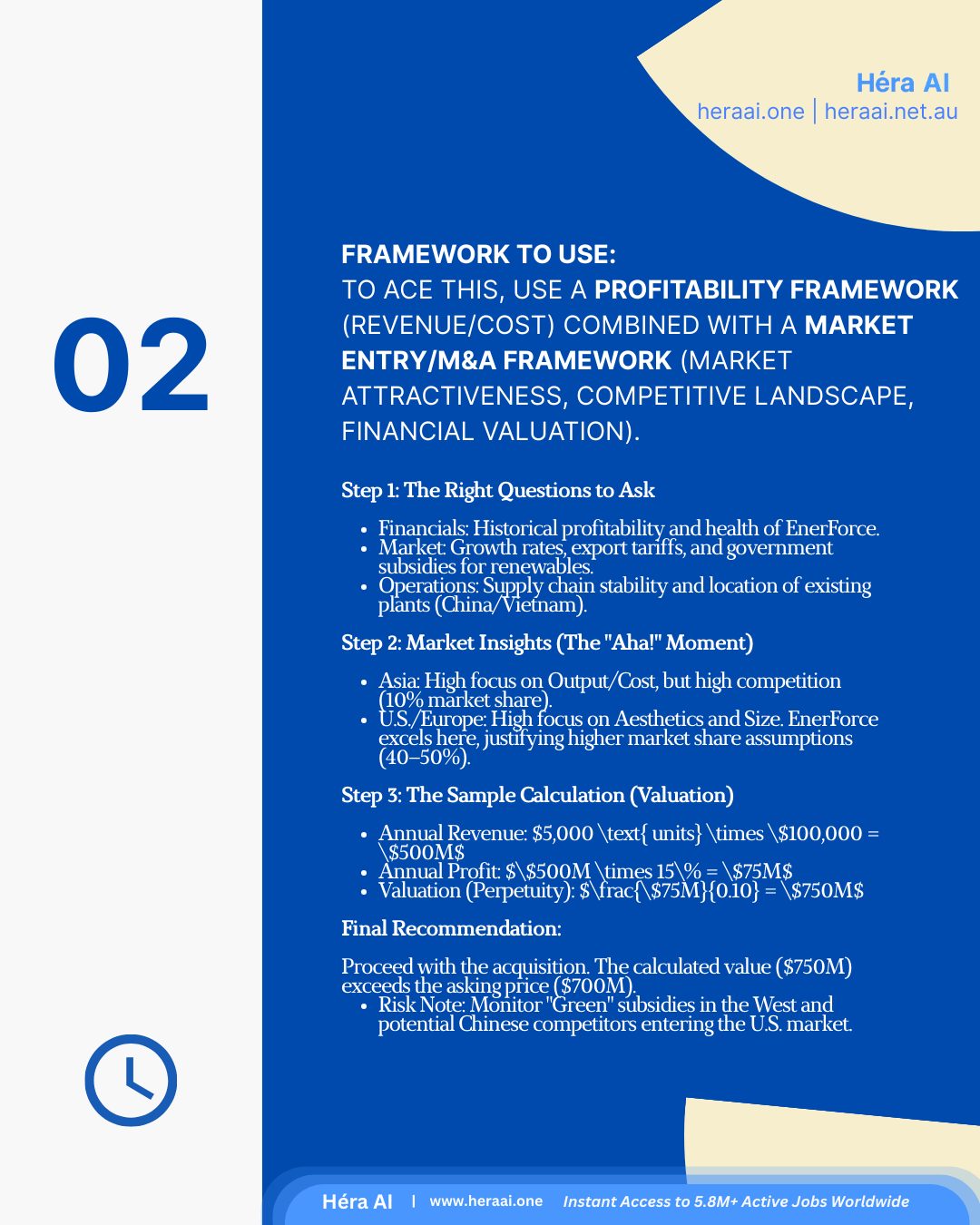

An M&A valuation is only as reliable as the due diligence that validates its inputs. In Case 15, the perpetuity model rests on three numbers: production capacity, profit margin, and discount rate. Each of these has a due diligence question behind it — and answering those questions before building the model is the move that separates a structured M&A analysis from a calculation exercise.

The question that must be asked before any revenue assumption is made: 'What is EnerForce's historical track record of operating at or near full production capacity?' A valuation built on 5,000 units per year is only valid if EnerForce has demonstrated the ability to actually sell and deliver 5,000 units. If the historical utilisation rate is 70–80%, the revenue base and the resulting valuation should reflect that — not the theoretical maximum.

The Market Insight: Asia vs. Western Markets Are Not Equivalent

The 'aha' moment in Case 15 is recognising that the two available markets for EnerForce's turbine respond to entirely different value propositions — and that the strategic implication is counter-intuitive: despite having manufacturing in Asia, EnerForce's most attractive market is the West. The table below maps the six dimensions that distinguish the two markets.

The counter-intuitive market insight that the case is designed to surface: Having manufacturing in China and Vietnam might suggest that Asia is EnerForce's natural primary market. The correct analysis reverses this assumption: Asia is where EnerForce manufactures, not where it will win market share. The domestic competition in Asia is too intense, and the purchase criteria (cost per output) favour local producers with subsidised cost structures. The Western market — where EnerForce's manufacturing origin is less visible and its product quality and aesthetics are more valued — is where the 40–50% share assumption is defensible. This is the market insight that distinguishes a candidate who reads the data from one who understands the dynamics.

The Perpetuity Valuation: Building the Model from First Principles

The valuation methodology for Case 15 is a perpetuity model — appropriate for a going-concern business in a growth sector where cash flows are expected to continue indefinitely. The model has three inputs: annual profit, and the discount rate that converts annual profit into a present value. Each input is derived from an assumption that should be named, not assumed.

The perpetuity formula — and why the $50M buffer deserves scrutiny: Valuation = Annual Profit ÷ Discount Rate = $75M ÷ 10% = $750M. The $50M gap between this figure and the $700M asking price looks like a comfortable margin of safety. It is not. A single-point reduction in the margin assumption — from 15% to 10% — reduces annual profit to $50M and the valuation to $500M, which is $200M below asking. A valuation with this level of sensitivity to a margin assumption that has not been stress-tested is a valuation that should not be trusted at face value.

Sensitivity Analysis: What Breaks the Deal

The base-case perpetuity valuation is $750M. But a valuation is not a fact — it is a model output that is only as reliable as its assumptions. The sensitivity analysis below tests four realistic downside scenarios against the base case and shows how quickly the $50M buffer can disappear.

The 5-Step Framework

The meta-lesson that Case 15 is designed to teach — applicable to every M&A valuation case: A valuation is a confidence interval, not a number. The $750M figure is the output of a base-case model with optimistic assumptions — 100% capacity utilisation, stable 15% margins, and full Western market pricing sustained in perpetuity. The stress tests show that three of four downside scenarios produce a valuation below the $700M asking price. The recommendation to proceed is not wrong — but it is conditional. The $50M buffer is not a safety net; it is the cost of the residual risk. A candidate who presents the $750M figure as a confident 'yes' without naming the conditions under which it becomes a 'no' has completed the calculation without completing the analysis.